The Evolution of the Wallet and the Rise of Minimalism

The history of the wallet is a reflection of economic history. In the early 20th century, wallets were primarily designed to carry paper currency. Following the introduction of the first universal credit card by Diners Club in 1950, wallet designs expanded to accommodate plastic. By the 1990s, the "Costanza wallet"—a term popularized by the sitcom Seinfeld to describe a wallet so overstuffed it causes physical discomfort—became a cultural touchstone for the excessive accumulation of physical clutter.

In the last decade, however, the trend has reversed. The shift toward digital payments, Apple Pay, and Google Wallet has allowed many to move toward "front-pocket wallets" or "minimalist cardholders." This transition is driven by two primary factors: ergonomics and security. Physicians have long warned that sitting on a thick wallet in a back pocket can lead to "wallet sciatica" or piriformis syndrome, a condition where the wallet compresses the sciatic nerve, causing chronic lower back and leg pain. Simultaneously, cybersecurity experts warn that the more information a physical wallet contains, the higher the "payload" for a thief.

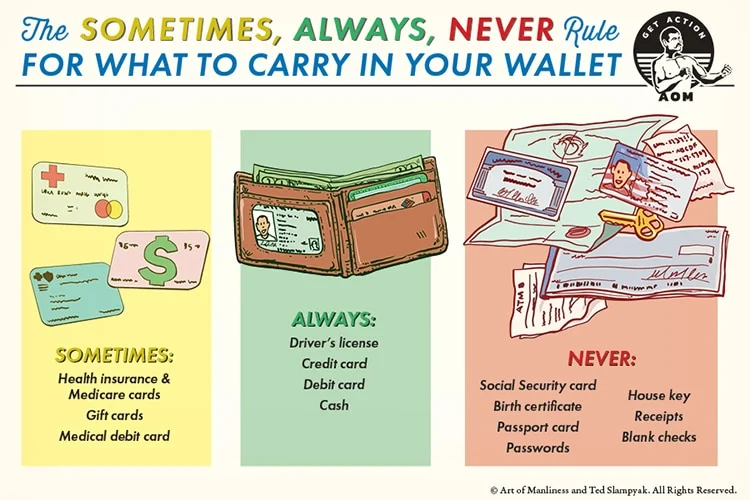

The "Always" Category: Essential Identification and Liquidity

According to security protocols and legal requirements, certain items must remain in the wallet at all times to ensure the owner can navigate daily life and emergencies.

1. Valid Driver’s License or Government ID

In nearly every jurisdiction, operating a motor vehicle requires the physical possession of a valid driver’s license. While several states have begun implementing "Digital IDs," law enforcement agencies generally recommend carrying the physical card as a backup, particularly when traveling across state lines where digital versions may not yet be recognized.

2. A Primary Credit Card

Financial advisors recommend carrying a single, high-limit credit card with robust fraud protection. Choosing a card with universal acceptance, such as a Visa or Mastercard, ensures that the user is never stranded. By carrying only one card, the user simplifies the process of freezing accounts should the wallet be lost.

3. A Debit Card

While credit cards offer better fraud protection for purchases, a debit card remains essential for ATM access. However, experts suggest that users should set low daily withdrawal limits and enable "push notifications" for every transaction to mitigate the risk of a compromised PIN.

4. Emergency Cash

Despite the "cashless" trend, recent data suggests that cash remains a vital tool for resilience. According to a 2023 Federal Reserve report on the Diary of Consumer Payment Choice, cash still accounts for approximately 18% of all payments and is the preferred method for small-value transactions under $10. Carrying between $100 and $300 in small denominations is recommended to handle cash-only businesses, tips, or situations where electronic payment systems are offline due to power outages or network failures.

The "Sometimes" Category: Strategic Inclusion Based on Utility

Items in the "sometimes" category are those that provide value only in specific contexts and represent a redundant risk if carried daily.

1. Health Insurance and Medicare Cards

Medical identity theft is a growing concern. The Federal Trade Commission (FTC) has noted that thieves can use stolen insurance information to receive medical treatments, which then become part of the victim’s permanent medical record, potentially leading to incorrect blood type entries or drug allergy misinformation. Hospitals are legally required to stabilize patients in emergencies regardless of whether they have their physical insurance card present. Therefore, these cards should only be carried when attending a scheduled medical appointment.

2. Gift Cards and Store Credits

Gift cards are essentially "bearer instruments," meaning whoever holds the card owns the value. Unlike credit cards, they cannot be easily frozen or replaced if stolen. Users should only place a gift card in their wallet when they have a specific intent to visit that retailer.

3. Medical Debit Cards (HSA/FSA)

Similar to health insurance cards, Health Savings Account (HSA) or Flexible Spending Account (FSA) cards are specialized tools. Carrying them daily increases the risk of loss without providing daily utility.

The "Never" Category: High-Risk Liabilities

The items in this category are those that facilitate identity theft or physical security breaches.

1. Social Security Cards and Birth Certificates

The Social Security Number (SSN) is the "skeleton key" to a person’s financial life. If a thief obtains a physical SSN card alongside a driver’s license, they have everything required to open new lines of credit, apply for loans, and file fraudulent tax returns. The Social Security Administration explicitly advises citizens to keep their cards in a secure, fireproof location at home rather than in a wallet.

2. Passwords and PINs

Writing down passwords for bank accounts or phone passcodes on a slip of paper in a wallet is a common mistake among the elderly and those with "password fatigue." However, this practice essentially hands a thief the keys to one’s entire digital and financial existence. Security experts advocate for the use of digital password managers with biometric locks instead.

3. House Keys

Carrying a spare house key in a wallet is a significant security flaw. Because a wallet almost always contains a driver’s license with a home address, a thief who steals a wallet with a key inside effectively has an invitation to the victim’s residence. If the wallet is stolen, the victim must not only cancel their cards but also immediately re-key their home.

4. Blank Checks

Blank checks contain a wealth of information, including the account holder’s name, address, bank routing number, and account number. A criminal can use this information to create forged checks or initiate unauthorized electronic transfers (ACH).

Chronology of Modern Wallet Security Standards

- 2005: The rise of RFID (Radio Frequency Identification) in credit cards leads to the popularity of "RFID-blocking" wallets to prevent "skimming."

- 2014: The launch of Apple Pay begins the widespread adoption of mobile wallets, reducing the need for physical cards.

- 2018-2022: Minimalist wallet brands like Ridge and Bellroy see a 200% increase in market share, signaling a shift away from traditional leather bifolds.

- 2023: The FTC reports that identity theft losses reached $10 billion, a 14% increase over the previous year, prompting new warnings about carrying sensitive documents.

- 2025 (Projected): More than 30 U.S. states are expected to offer some form of digital driver’s license, further reducing the necessary contents of a physical wallet.

Supporting Data: The Cost of a Lost Wallet

The impact of losing a wallet goes beyond the loss of physical cash. According to a study by Javelin Strategy & Research, the average victim of identity fraud spends approximately 7 to 10 hours resolving the issues stemming from the theft. If a Social Security card is involved, that time can balloon to over 40 hours of administrative labor, including visits to the DMV, the Social Security office, and various banking institutions.

Furthermore, the physical cost of "George Costanza" wallets is measurable. A study published in the Journal of Physical Therapy Science found that sitting on a wallet as thin as 10mm (about 0.4 inches) can cause a significant pelvic tilt, leading to compensatory spinal curvature and long-term musculoskeletal issues.

Official Responses and Expert Analysis

Cybersecurity analysts from firms such as Norton and McAfee consistently emphasize that "physical security is the first line of defense for digital security." When a wallet is lost, the "Always/Sometimes/Never" rule acts as a damage mitigation strategy.

"The goal is to minimize the ‘blast radius’ of a lost wallet," says Marcus Thorne, a senior consultant at a leading cybersecurity firm. "If you only carry one credit card and no sensitive documents, you can secure your entire financial life with one phone call. If you carry your Social Security card and multiple checks, you could be fighting the fallout for a decade."

Law enforcement officials also support the minimalist approach. "We often see victims who can’t even remember how many credit cards were in their wallet when it was stolen," notes Sergeant Elena Rodriguez of the Metropolitan Police Department. "A streamlined wallet allows for a faster, more accurate police report, which increases the chances of flagging the stolen items before they are used fraudulently."

Broader Impact and Implications for the Future

The "Sometimes Always Never" rule is more than a guide for organization; it is a response to a world where data is as valuable as currency. As we move toward 2030, the physical wallet may eventually be relegated to a ceremonial or fashion accessory, with the majority of its functions absorbed by biometric-secured smartphones and wearables.

Until that digital transition is total, the physical wallet remains a critical bridge between the analog and digital worlds. By adhering to a strict regimen of what to carry, individuals can protect their posture, their peace of mind, and their financial future. The reduction of the wallet’s profile is a symbolic move toward a more intentional and secure way of living, proving that in the realm of personal security, less is almost always more.